Out-of-pocket imaging cost breakdown is the detailed accounting of every fee a self-pay or uninsured patient incurs for medical imaging procedures such as MRI, CT scans, and X-rays. These costs include the technical component, professional radiologist fees, facility charges, and add-ons like contrast dye. The total varies widely depending on the type of scan, the facility you choose, and your geographic location. Understanding this breakdown before you schedule a scan is the most direct way to avoid surprise bills and overpaying by hundreds or even thousands of dollars.

What components make up your out-of-pocket imaging bill?

Every imaging bill contains multiple line items, and most patients receive more than one statement. Imaging costs include the technical component, professional interpretation by radiologists, facility fees, contrast dye, and additional charges for image copies or rush reports. Knowing what each charge represents gives you the ability to question it, compare it, and negotiate it.

The technical component covers the actual operation of the scanner, the equipment use, and the technician's time. This is typically the largest single charge on your bill.

The professional component is a separate fee billed by the radiologist who reads and interprets your images. This charge often arrives as a second, independent bill days after your scan. Many patients are caught off guard by it.

Facility fees reflect the overhead costs of the building, staff, and administrative systems. Hospitals charge significantly higher facility fees than freestanding imaging centers because their overhead is far greater.

Contrast dye is an injectable substance used to improve image clarity for certain scans. Contrast dye adds $100 to $400 to the total cost, covering the dye itself, IV setup, and nursing administration. Contrast is only ordered when clinically indicated, so always confirm with your ordering provider whether it is necessary for your specific scan.

Additional charges can include fees for a CD copy of your images, rush report fees if results are needed quickly, and administrative processing fees. These are often small but worth asking about upfront.

Pro Tip: Request an itemized estimate before your appointment. Ask specifically whether the quote includes both the technical and professional components, or only one. Many facilities quote only the technical fee, leaving the radiologist bill as an unexpected second charge.

How do imaging costs vary by facility type and location?

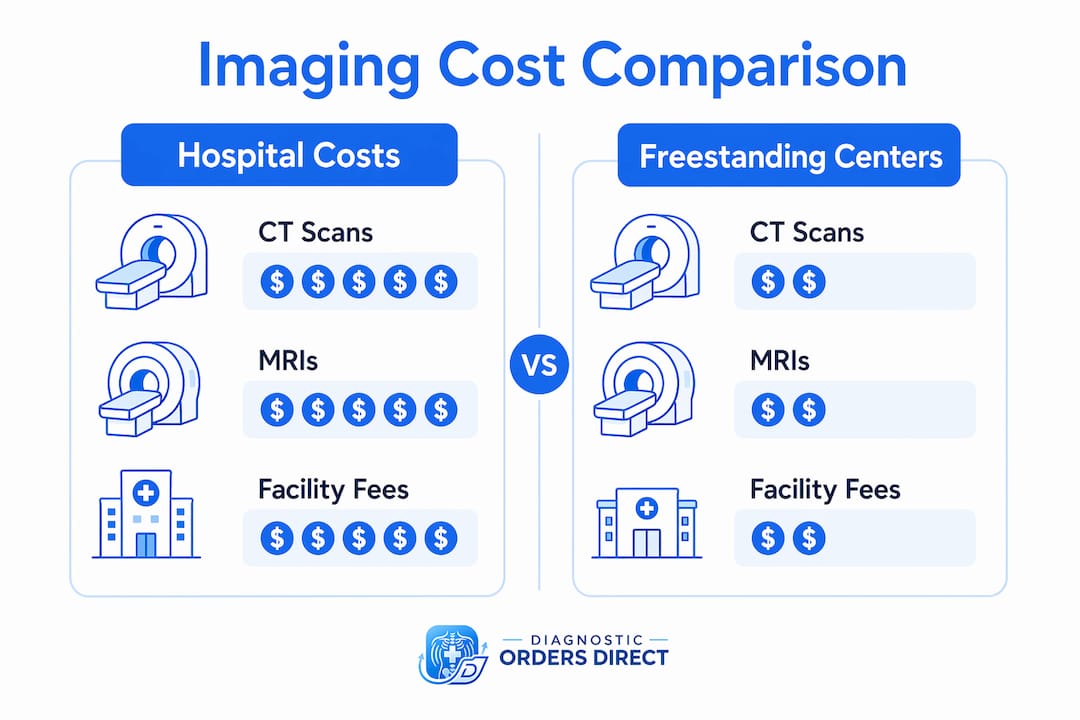

Facility type is the single biggest driver of cost variation in out-of-pocket medical imaging. CT scans at freestanding imaging centers cost between $250 and $2,000 without insurance, while hospitals charge $500 to over $7,000 for the same scan. That gap exists because hospitals carry far higher administrative overhead, maintain emergency infrastructure, and bill at inflated "chargemaster" rates.

The table below shows typical cash-pay price ranges by facility type and scan category.

| Scan type | Hospital (cash pay) | Freestanding imaging center |

|---|---|---|

| CT scan (without contrast) | $500 to $3,275 | $250 to $800 |

| CT scan (with contrast) | $800 to $7,000+ | $400 to $2,000 |

| MRI (without contrast) | $1,000 to $5,000 | $400 to $1,500 |

| MRI (with contrast) | $1,500 to $5,000+ | $600 to $2,500 |

| X-ray | $150 to $1,000 | $50 to $300 |

MRI self-pay costs range from about $400 to $5,000 or more, with averages around $1,300 to $2,000 at hospitals. Independent imaging centers charge significantly less, and assistance programs can bring the median cost down to $301. That is not a rounding error. It reflects a genuine structural difference in how these facilities price their services.

Geographic location adds another layer of variability. Urban markets in states like California, New York, and Massachusetts consistently show higher imaging prices than rural markets in states like Arkansas, Mississippi, or Iowa. A brain MRI that costs $2,200 at a hospital in San Francisco may cost $650 at a freestanding center in a mid-sized Midwestern city.

Pro Tip: Search for Radiology Benefit Managers or independent diagnostic testing facilities (IDTFs) in your area. These facilities are accredited, use the same equipment as hospitals, and charge a fraction of the price. Your primary care doctor or Diagnosticordersdirect can direct you to these centers.

What practical strategies can self-pay patients use to reduce imaging expenses?

The most effective way to avoid overpaying for imaging is to shop around and request cash prices directly from multiple facilities before booking. Research shows patients who skip this step ignore an average of six lower-priced centers before their appointment. That oversight can cost $1,000 or more on a single scan.

Here is a step-by-step approach to managing your imaging expenses breakdown:

-

Get your CPT code. The Current Procedural Terminology (CPT) code is the standardized billing code for your specific scan. Always verify the exact CPT code and whether the quote includes all necessary components. Without it, you cannot make accurate price comparisons between facilities.

-

Call at least three facilities. Contact hospitals, outpatient imaging centers, and freestanding radiology centers. Ask each for their self-pay or cash-pay price for your specific CPT code, with and without contrast.

-

Request a Good Faith Estimate. Good Faith Estimates are legally required written quotes that detail expected out-of-pocket costs for imaging procedures. Request one before any non-emergency scan. It gives you a written, defensible number to reference if the final bill is higher.

-

Ask about self-pay discounts. Hospitals offer self-pay discounts of 15% to 50% when patients request cash prices before the procedure. Hospitals prefer upfront payment over chasing insurance claims, so this negotiation is standard practice, not an exception.

-

Confirm whether contrast is required. Ask your ordering provider directly whether contrast is clinically necessary for your scan. If it is not, removing it saves $100 to $400 immediately.

-

Ask about payment plans. Most facilities offer interest-free payment plans for self-pay patients. This does not reduce the total cost but prevents a large single payment from becoming a financial crisis.

-

Use price comparison tools. Platforms like Healthcare Bluebook and FAIR Health Consumer allow you to look up fair-price benchmarks for imaging procedures in your zip code. These tools give you a credible reference point when negotiating.

Pro Tip: When calling for quotes, say "I am a self-pay patient and I need your cash price for CPT code [your code]." This phrasing signals that you are informed and prompts billing staff to give you the actual discounted rate rather than the standard chargemaster price.

How does insurance status affect your imaging cost?

Insurance does not automatically mean lower costs for imaging, particularly for patients with High-Deductible Health Plans (HDHPs). Unmet deductibles in HDHPs may cause insured patients to pay more than cash prices at independent imaging centers. This happens because the hospital bills the insurer at full rates, and those charges are applied to your deductible before any coverage kicks in.

The table below outlines how insurance status affects what you actually pay.

| Patient scenario | How cost is calculated | Typical outcome |

|---|---|---|

| Uninsured, pays cash at imaging center | Cash-pay rate negotiated directly | Lowest total cost in most cases |

| Insured, deductible not met | Full negotiated rate applied to deductible | Often equals or exceeds cash-pay price |

| Insured, deductible met | Coinsurance applies (typically 20% to 30%) | Lower cost if scan is expensive |

| Insured, out-of-pocket max reached | Insurance covers 100% | No cost to patient |

| Insured, out-of-network facility | Full billed rate may apply | Highest potential cost |

Key factors to understand before scheduling:

- Coinsurance is the percentage you pay after meeting your deductible. A 20% coinsurance on a $3,000 hospital MRI means you pay $600, which may still exceed the $400 cash price at a freestanding center.

- Out-of-pocket maximum is the annual cap on what you pay. Once reached, your insurer covers 100%. Imaging costs count toward this cap only when billed through insurance.

- Network status determines whether your insurer's negotiated rates apply. Out-of-network imaging can trigger full billed charges with no discount.

The practical takeaway: if your deductible is not yet met and you need a scan at a freestanding imaging center, calling to ask for the cash price and comparing it to your insurance's cost-sharing estimate is a direct way to determine which path costs less. Many self-pay patients with partial insurance coverage find that paying cash at independent centers saves money in the first half of the plan year.

Key takeaways

Understanding your imaging expenses breakdown before scheduling a scan is the most direct way to control costs, avoid surprise bills, and choose the right facility for your situation.

| Point | Details |

|---|---|

| Know your bill components | Every imaging bill includes technical fees, radiologist fees, facility fees, and potential contrast charges. |

| Facility type drives cost | Freestanding imaging centers charge 50% to 90% less than hospitals for identical scans. |

| Get your CPT code first | Accurate price comparisons require the specific CPT code for your scan before calling facilities. |

| Request a Good Faith Estimate | This legally required written quote protects you from surprise bills after the procedure. |

| Insurance is not always cheaper | Patients with unmet deductibles often pay less by using cash-pay rates at independent centers. |

What I've learned about imaging costs that most patients find out too late

Most patients walk into an imaging appointment the same way they walk into a grocery store without a list. They accept the first price they are given, assume insurance will handle it, and open the bill three weeks later with no frame of reference for what any of the charges mean.

The biggest mistake I see is patients treating imaging as a single transaction when it is actually three or four separate ones. The facility bill, the radiologist bill, the contrast charge, and the image copy fee all arrive independently. By the time the last statement shows up, the patient has already moved on mentally and is less likely to question anything.

The second mistake is assuming that having insurance means paying less. For anyone in the first half of a plan year with a $3,000 or $5,000 deductible, the math often works against them. A $400 cash-pay MRI at a freestanding center beats a $1,300 negotiated hospital rate applied to an unmet deductible every time.

The patients who manage imaging costs well share one habit: they ask questions before the scan, not after. They get the CPT code, call three facilities, request a Good Faith Estimate, and confirm whether contrast is actually necessary. That process takes about 30 minutes and can save $500 to $2,000 on a single procedure.

Healthcare pricing is not transparent by default. You have to request transparency directly. The tools exist. The legal protections exist. The discounts exist. They just do not come to you automatically.

— Tod

How Diagnosticordersdirect simplifies self-pay imaging orders

Self-pay patients face two obstacles: getting an imaging order and then managing the cost of the scan itself. Diagnosticordersdirect removes the first obstacle entirely.

Through a licensed provider consultation for just $40, Diagnosticordersdirect issues imaging orders for MRI, CT scans, and other diagnostics based on your symptoms and medical history. No primary care referral required. No insurance authorization delays. The platform connects patients directly to freestanding imaging centers nationwide, where cash-pay prices are a fraction of hospital rates. If you need to order imaging before a specialist appointment or simply want to move forward without waiting on a referral, Diagnosticordersdirect provides a direct, cost-effective path. Visit Diagnosticordersdirect to get started.

FAQ

What is included in an out-of-pocket imaging cost breakdown?

An out-of-pocket imaging cost breakdown includes the technical component, professional radiologist interpretation fee, facility fee, contrast dye charges if applicable, and any additional fees for image copies or rush reports. These charges often arrive as separate bills from different providers.

How much does an MRI cost without insurance?

MRI costs without insurance range from approximately $400 at freestanding imaging centers to $5,000 or more at hospitals, with the national average falling between $1,300 and $2,000. Assistance programs and cash-pay discounts can reduce costs significantly below these figures.

Is it cheaper to pay cash for imaging instead of using insurance?

For patients with unmet high-deductible plans, paying cash at a freestanding imaging center is often cheaper than using insurance, because the hospital bills the insurer at full rates that are applied to the deductible before any coverage applies. Comparing the cash price to your insurance's cost-sharing estimate before scheduling is the most reliable way to determine which option costs less.

What is a Good Faith Estimate and how does it help self-pay patients?

A Good Faith Estimate is a legally required written quote that details expected out-of-pocket costs for imaging procedures before the service is performed. It gives self-pay patients a documented price to reference if the final bill is higher than expected.

How can I find lower imaging costs in my area?

Request the CPT code for your scan from your ordering provider, then call at least three facilities including freestanding imaging centers and ask for their cash-pay price. Tools like Healthcare Bluebook and FAIR Health Consumer provide regional price benchmarks to help you evaluate whether a quoted price is reasonable.